2025 in Review: What Mattered And What’s Next

A handful of closing bells to go in 2025.

The market’s positive momentum from 2024 promptly carried into January as investors remained optimistic on everything AI and a pro-business administration focused on the potential of deregulation. The first real test of the year came on January 27th — a.k.a. DeepSeek Monday. The Chinese AI company released its chatbot which led to a sharp drawdown in global technology stocks. Investors worried that the AI hardware and large-model business architype might be disrupted with significantly cheaper (yet still efficient) models like DeepSeek potentially having the ability to knock off some of the biggest players. However, these fears turned out to be relatively short-lived as the AI complex quickly regained its footing and soared higher over the course of the year (with some volatility along the way).

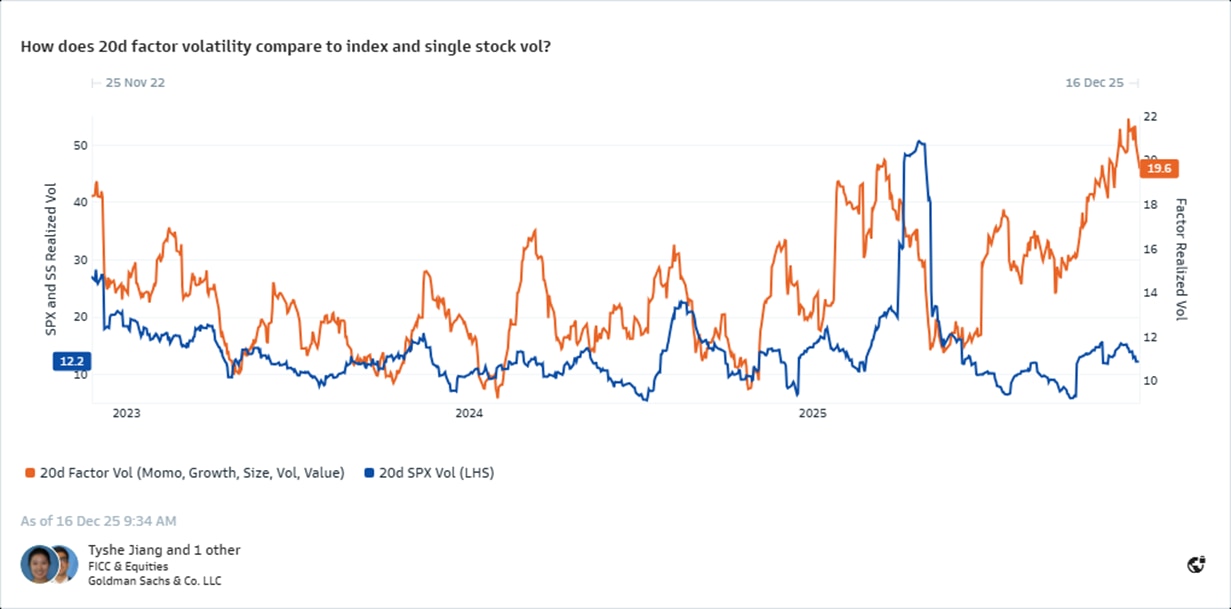

Due to a bout of extreme factor volatility March 7 and March 10 will go down as one of the worst two-day stretches of hedge fund performance in years (multistrat-mageddon). The momentum factor experienced a 4+ standard deviation drawdown which led to forced derisking across various types of HF strategies. Fortunately this episode led to cleaner positioning as traders braced to enter the second quarter...

Source: Marquee MarketView, as of 16 December 2025.

President Donald Trump’s “Liberation Day” will be remembered as the most impactful event for the U.S. stock market in 2025. After the market close on April 2, the president announced wide-ranging new tariffs on imports at unexpectedly high rates. The S&P 500 promptly lost 13% from April 3 to April 8 and closed sub 5,000 on April 8, which was good for the low close of the year.

However, on April 9 Donald Trump announced a 90-day pause on tariffs causing the S&P 500 to experience its sharpest intraday reversal since 2008 (the index closed +952bps on the day). This set the stage for the S&P 500 to make 33 additional record closes in 2025 (there have been 36 total this year and I think there are several more to come over the next 3 weeks).

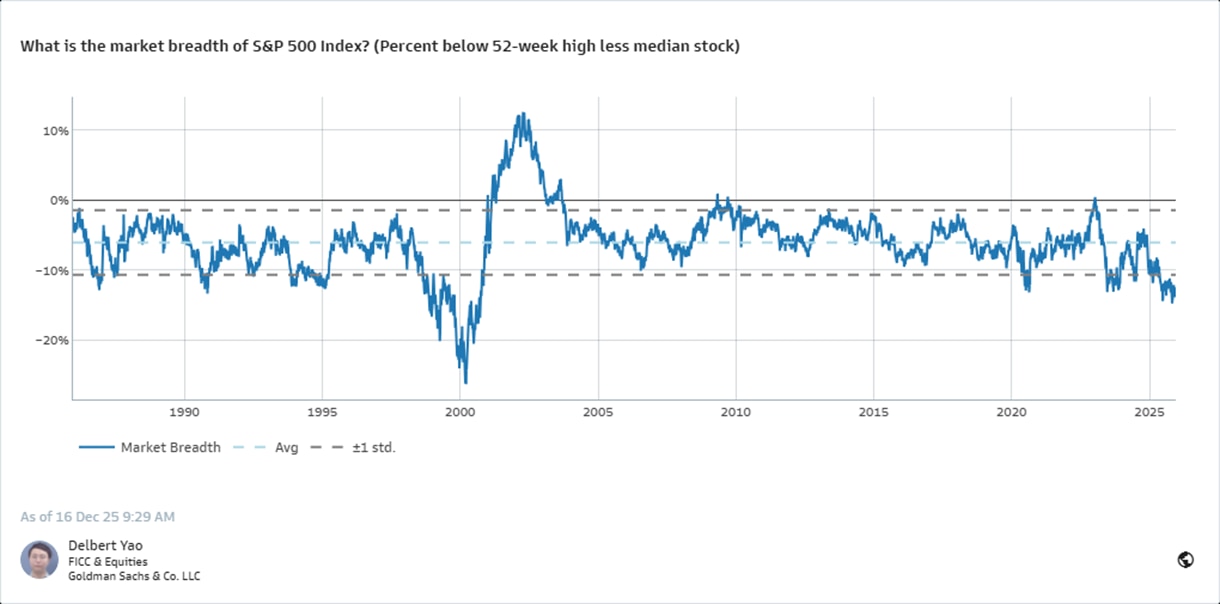

Desk flows and conversations suggest that post-Liberation Day, a great majority of professional institutional investors remained skeptical of the market’s rally and stayed on the sidelines. The most common reasons cited for this skepticism were geopolitical/macro/policy uncertainty, rich valuations, and poor market breadth. As a result, fundamental L/S HF net exposure has spent most of the year well below the 50th percentile rank on 1, 3 and 5-year lookbacks. MFs sat on a significant amount of cash until the fourth quarter (too late). Only 28% of large-cap mutual funds are outperforming their benchmarks (the lowest share since 2019). The average fundamental long-short HF is underperforming the S&P 500 by ~200bps. Our sentiment indicator has spent most of the year in negative territory reflecting relatively light institutional investor positioning. The wall of worry has been extremely high this year and remains omnipresent (bullish signal).

Source: Marquee MarketView, as of 16 December 2025.

Three investor cohorts that have shown up as noteworthy buyers of U.S. stocks this year are the retail community, corporates, and foreigners. Our data shows that the well-informed retail community now only consistently sells stocks when there is significant job loss (as in March of 2020). The retail cohort’s most significant buy imbalances were in early April post-liberation day. Retail got it right.

Companies have once again repurchased over $1T of their shares in 2025 making it a top 3 buyback year in the history of the stock market. As authorizations continue to ramp, I believe $1T annual corporate bids will be the new norm on the go forward (recessions aside). Both retail and corporates have provided a higher floor for the market at the index level continuing to frustrate the HF and MF communities.

Even as the markets appeared to question U.S. exceptionalism throughout the year, foreign investors have been the single largest source of U.S. equity demand YTD. Foreign investors bought nearly $280 billion in May and June this year, continuing the usual pattern of elevated foreign investor demand after the dollar has weakened and U.S. equities have underperformed.

During the front half of the year we saw several U.S. institutional investors build significant longs in select European equities for the first time in years. However, this demand has not carried into the back half of the year. I worry that when things get hard again these stocks will be the first out the door in a LIFO (last in, first out) phenomenon. Away from the U.S., investors are currently doing most of their work on Brazil, Korea, and India. I believe Brazil is primed to have a moment in 2026 if a rate-cutting cycle coincides with a change election, leading to a potential re-rating in Brazilian assets. China remains uncertain.

Lower rates, a weaker USD, a resilient consumer, solid earnings, 2% GDP growth, and cautious sentiment make me believe the U.S. stock market will be the best place to be in 2026. Our trading desk expects companies with high-floating-rate debt to benefit from lower rates. Currently, the trailing 12-month interest expense makes up ~70% of next 12-month EBIT estimates and as floating rate debt re-rates lower, this could directly boost earnings.

GIR’s baseline economic forecast is that growth reaccelerates to 2-2.5% in 2026 because of reduced tariff drag, tax cuts, and easier financial conditions. Standard models suggest that this should boost job creation and stabilize the unemployment rate at a level only modestly above September’s 4.44%. Under this forecast, our working assumption is that the FOMC slows the pace of easing in 2026H1, pausing in January but still delivering two more cuts in March and June which push the funds rate down to a terminal level of 3 - 3.25%.

From my trading seat, an average of 17.5 billion shares traded across the U.S. equity market each day this year. For context, this number was 10.8 billion shares in 2020. However, trading has never been more difficult as liquidity is hard to come by as this volume growth is happening off-exchange which traders cannot access. Over 75% of off-exchange volume now trades in OTC market centers, which includes retail flow mostly inaccessible to institutional investors. Fragmentation in the U.S. markets poses further challenges with 16 exchanges, over 30 ATSs and hundreds of OTC liquidity destinations. The average trade size has dropped both on and off exchange, reaching a 15-year low this year of ~150 shares per trade. “Knowing where the bodies lie” has never been more important.

Per the usual, we must be mentally prepared for several macro scares next year, but latest data from company earnings strengthens the argument that Corporate America has room to grow. Not to mention the M&A spike we witnessed this year should accelerate next year as companies capitalize on a more permissible regulatory backdrop and seek out cost synergy opportunities to offset persistent macro pressures. The IPO market seems promising as well. The Retail bid should remain strong as tax refunds spike in early 2026 (2025 were never adjusted to reflect OBBBA and therefore many will be due a large refund). Throwing these dynamics into a blender makes me believe the S&P 500 has a very viable path to 7800 next year. My favorite trade for 2026 is getting long some of the more under-the-radar AI productivity beneficiaries.

The names "Goldman Sachs," and "Marquee" are the trademarks or registered trademarks of Goldman Sachs.

© 2026 Goldman Sachs & Co. LLC. All rights reserved. Descriptions of the products and services available through the Marquee platform provided herein are for educational purposes only and do not reflect all information that may be relevant in determining whether use of any such product or service is suitable for your circumstances. Goldman Sachs is not recommending that you take any action based on any information presented herein, which may be updated or modified form time-to-time by Goldman Sachs in its sole discretion without prior notice or subsequent notification. Prior to utilizing product or service available through the Marquee platform, you should read carefully any related disclosure provided by Goldman Sachs, including any information to which you may be required to agree and acknowledge or any user agreements that you may be required to execute, and make an independent determination regarding the suitability of your use of the relevant product or service.

The reference to or appearance of another company’s name, trademark, or logo in these materials / on this site does not constitute or imply, and is not intended to constitute or imply, any type of affiliation, endorsement, sponsorship, approval, or the like by or between such company and Goldman Sachs or any of their respective products, services, or affiliates. Any such reference or appearance is made for informational purposes. All such names, marks, and logos are the intellectual property of their respective owners.